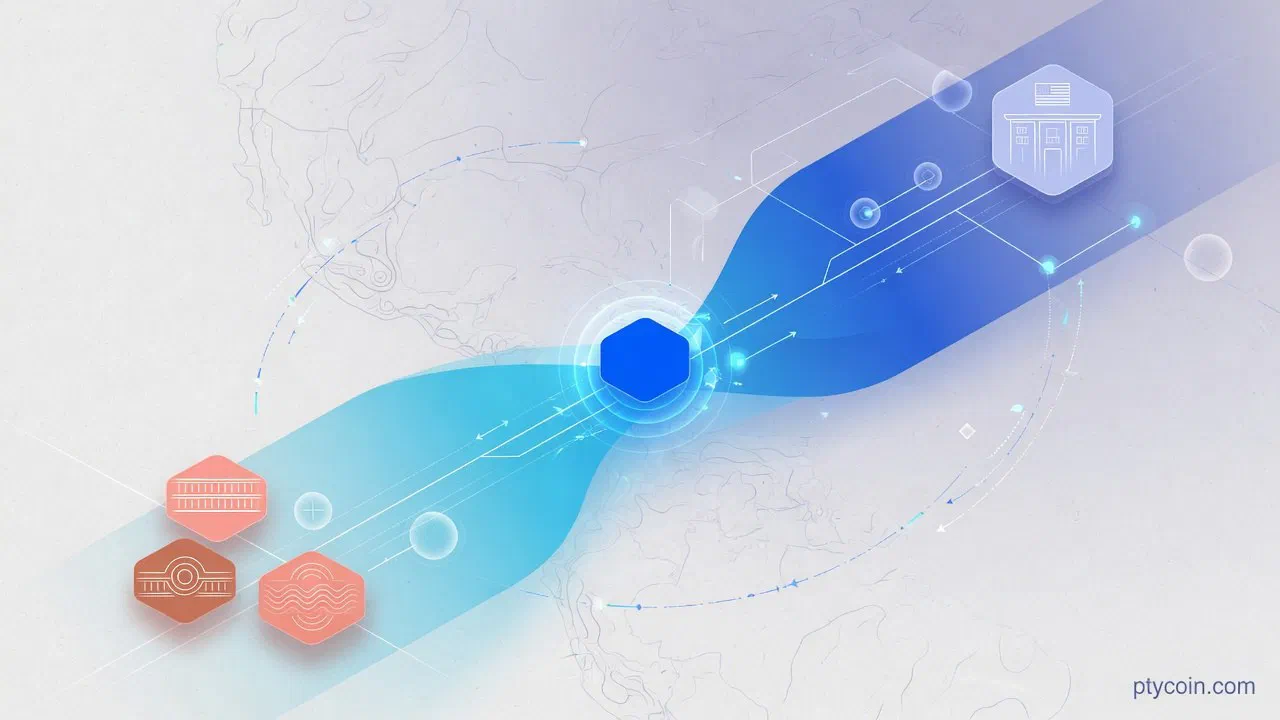

Fintechs and payment service providers (PSPs) moving money between the US and Latin America have long juggled fragmented rails, pre-funding requirements, and compliance overhead that slows everything down. BlindPay offers an API that lets companies send and receive using stablecoins for the cross-border portion while connecting directly to local instant systems — Pix in Brazil, SPEI in Mexico, and equivalents elsewhere — without forcing either side to become a crypto treasury operator.

The company, founded by veterans of Brazil’s largest fintechs, recently added AI-assisted document review, GDPR compliance, and SEPA payouts, positioning it as infrastructure that works for both LatAm corridors and expanding global flows.

Context: the persistent friction in US–LatAm corridors

Traditional correspondent banking still dominates many business payments into and out of Latin America. A US company paying contractors or suppliers in Brazil, Mexico, or Colombia faces multi-day settlement windows, FX spreads that are rarely transparent, intermediary deductions, and the operational burden of maintaining relationships or pre-funded accounts across markets.

Domestic instant payment systems in the region are fast and cheap inside country borders, but they stop at the border. Moving value from a US bank account to a Brazilian Pix recipient the old way still incurs the international premium in time and cost. Stablecoins emerged as a practical settlement layer precisely because they settle 24/7 on public ledgers with low fees and atomic finality, while the fiat on- and off-ramps stay with licensed local partners.

Surveys have placed Latin America at the leading edge of stablecoin adoption for exactly these cross-border and treasury use cases. The practical question for builders is which APIs make the hybrid model — stablecoin bridge plus local rail last mile — reliable and compliant enough to use in production.

How BlindPay works

BlindPay exposes a unified REST API plus SDKs (TypeScript, Python, PHP, Swift, Go) for orchestrating pay-ins and payouts that can start or end in fiat or stablecoins. Two core flows stand out.

For payouts (e.g., paying a Brazilian contractor from USD or stablecoins): the sender approves a transfer of USDC (or supported stable) from their own wallet via standard ERC-20 approval on supported chains. BlindPay collects the tokens, converts at a quoted rate, and delivers the local currency through the destination rail — Pix, SPEI, or others. If the fiat leg fails, the stablecoins are returned to the originating wallet. The platform emphasizes this non-custodial character for the on-chain leg: funds remain under user control until the explicit approval step.

For pay-ins (receiving USD or other fiat and getting stablecoins out): users can deposit into named virtual accounts issued through a Tier-1 US banking partner. The account appears in the recipient’s name on statements. Deposits trigger automatic conversion to the chosen stablecoin and delivery to a specified wallet address. This removes the need for a US entity just to receive dollar payments.

Named virtual accounts support ACH, Wire, and SWIFT. The same API surface handles KYC/KYB onboarding, limit requests, transaction monitoring, and webhooks for real-time status. Recent additions include SEPA payouts to EUR bank accounts across dozens of countries (with multi-chain support) and the ability to request quotes denominated in the output currency.

Compliance is built in at multiple layers: automated screening, document verification, on-chain monitoring, and local regulatory alignment. The company is registered as an MSB with FinCEN. Every virtual account and higher-volume flow goes through compliance review.

Analysis: team, product velocity, and honest limits

BlindPay was incorporated in Delaware in May 2024. The team is heavily LatAm-rooted. CEO Bernardo Simonassi previously built the first payroll platform powered by stablecoins and worked on instant payments at PicPay (serving 60M+ users). COO João Borges founded a major Brazilian blockchain startup, scaled it to seven-figure revenue, and is a Forbes 30 Under 30 honoree. CPO Gustavo Marinho also came from PicPay, where he led loans and instant payment products. The engineering side includes experience from LendingClub and AWS.

In 2025 the company raised a $3.3M seed round backed by Y Combinator (W25), 468 Capital, Bitso Business, Transpose Platform, Acacia Venture Capital, and angels including YouTube co-founder Jawed Karim.

Public volume figures are not disclosed at the scale Conduit has shared, which is typical for an earlier-stage infrastructure player. What is visible is rapid product iteration: the changelog shows SEPA EUR payouts in late May 2026, multi-chain and EUR-amount quote support in early June, and on June 14 a new AI Document Analysis endpoint that pre-screens KYC files and returns an approval-rate signal before submission. On June 17 the CEO announced GDPR compliance, framing it as part of becoming “the most enterprise-ready stablecoin API for global payments.”

Honest caveats:

Like most API-layer providers, final speed and cost still depend on the quality and pricing of the licensed on/off-ramp partners at each end. BlindPay orchestrates; it does not replace those rails.

Compliance reviews for virtual accounts and certain flows add a human step that can introduce short delays, even if the company advertises fast SLAs in many cases.

Self-custody is supported on the payout side via wallet approvals and on the receive side via direct stablecoin delivery, but businesses that want fully hands-off operation will rely on the platform or its partners for parts of the flow. The product is explicitly built for companies that may already hold or want to receive stablecoins in their own wallets.

Early-stage infrastructure carries execution risk around liquidity in thinner corridors, operational resilience under volume spikes, and keeping pace with regulatory changes across many jurisdictions.

No single on-chain “BlindPay protocol” is the product; the value is the orchestration layer, the partner network, the compliance surface, and the developer tooling (including recent CLI and AI/MCP integrations for agents).

The developer experience and AI-native tooling are real differentiators. Besides the core SDKs, there is a CLI, “Agent Skills” that teach AI assistants the API surface, and an MCP server that lets compatible AI tools call the API directly.

Why Latin America cares

Latin American fintechs and PSPs often serve users who expect instant local payouts (Pix is the default in Brazil) while needing to accept or disburse dollars or other currencies for cross-border work, marketplaces, remittances, or payroll. Building the full stack of virtual accounts, compliance, multi-rail routing, and stablecoin handling in-house is expensive and slow.

BlindPay’s Brazilian founding team and explicit focus on the corridors that matter — US to Brazil/Mexico/Argentina/Colombia and back — means the integrations with local methods are native rather than bolted on. A marketplace operator in São Paulo or a payroll platform serving freelancers across the region can add global payout and collection capabilities through one API instead of stitching together banks, FX desks, and separate stablecoin providers.

The self-custody angle matters here. When a platform or its users already manage stablecoin balances (common in LatAm for hedging or cross-border treasury), BlindPay lets them move value on-chain with finality and then cash out locally without surrendering the entire flow to a custodian. For companies uncomfortable with on-chain keys, the virtual account and automated conversion paths still deliver the speed and cost benefits.

Recent expansions beyond pure LatAm (SEPA, GDPR) also help LatAm companies that want to pay or receive from Europe without adding another vendor. The AI tooling can reduce the manual compliance burden that disproportionately affects smaller regional players.

The 2026 regulatory backdrop helps too: defined frameworks for stablecoin FX in Brazil and emerging US federal rules for payment stablecoins reduce some of the gray area that made earlier experiments riskier.

Takeaway

BlindPay is a concrete example of the maturing layer of stablecoin infrastructure purpose-built for the payment flows that actually dominate Latin America’s digital economy — not speculative trading, but payouts to contractors, supplier settlements, marketplace disbursements, and cross-border freelance work.

Its combination of named virtual accounts, direct local-rail handoff, wallet-native flows, and accelerating developer and AI tooling makes the “stablecoin sandwich” practical for teams that do not want to become blockchain specialists. The recent cadence of features (AI pre-screening, SEPA, GDPR) shows a team shipping to close real operational gaps.

That said, it is still an early-stage company. Businesses should validate end-to-end economics and reliability on the specific corridors and volumes they care about, review the compliance model and partner dependencies, and treat any cost or time savings claims as starting points for their own modeling rather than guarantees. No single provider eliminates all friction or risk in global payments.

For LatAm fintechs, PSPs, and platforms that move money regularly across borders, BlindPay is worth a direct integration test or pilot. The API surface and recent tooling lower the barrier to trying the model without a massive engineering commitment. As with any treasury or payments infrastructure choice, run the numbers on your own flows and counterparties.

This is not financial advice. The right rail is the one that matches your corridors, compliance needs, custody preferences, and volume profile.

Sources

- BlindPay website, docs, changelog, and compliance (FinCEN MSB registration).

- BlindPay — Y Combinator company profile (W25) and the YC launch post.

- “LATAM Corridor Economics: Why Enterprises Are Betting on Stablecoins for Cross-Border Payments,” Polygon blog, March 6, 2026.

- “BlindPay raises $3.3M to expand operations,” LatamList, August 2025.

- BlindPay SDKs and tooling on GitHub (blindpaylabs) — TypeScript, Python, PHP, Swift, Go, plus MCP server.

- CEO Bernardo Simonassi’s GDPR-compliance announcement on X (June 17, 2026).