In countries where local currencies lose value quickly or capital controls make dollars scarce, millions turn to stablecoins as practical digital dollars. El Dorado packages that access into a single consumer superapp with P2P marketplaces, named dollar accounts, QR payments, and on/off ramps that feel native to each country. A recent $9 million Series A led by Paradigm, with Coinbase Ventures and Verda Ventures, gives the company fresh capital to expand its footprint and launch a business offering built on Tempo, a payments-focused Layer 1 incubated by Paradigm and Stripe.

Context: dollars without the bank

Latin America has world-class domestic instant payments inside borders — Pix in Brazil, SPEI in Mexico, Yape and others elsewhere — but moving value across them or into dollars has historically meant slow wires, wide FX spreads, and accounts that are hard to open or keep stable. For freelancers receiving foreign payments, families receiving remittances, or anyone trying to preserve purchasing power in high-inflation or restricted environments, the friction is real and recurring.

Stablecoins emerged as the working solution because they deliver dollar parity with internet speed and visible finality on public chains. P2P markets flourished where official channels were expensive or restricted. The missing piece was an app that made the full loop — local fiat in, stablecoin hold or transfer, local fiat or spend out — feel as simple as a domestic payment app, without requiring users to manage keys, bridges, or exchanges themselves.

El Dorado positions itself as that layer: a “Money SuperApp” that keeps the stablecoin rails under the hood while the interface speaks the language of each country’s familiar payment methods.

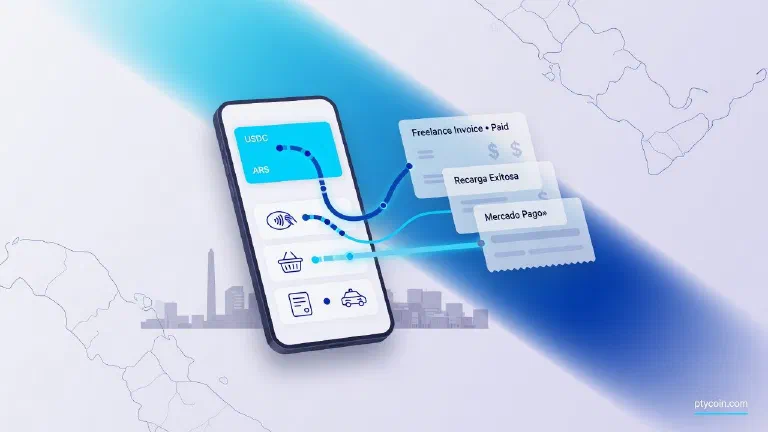

How El Dorado works

The app organizes features into Mini Apps. Core offerings today include:

P2P marketplace: Buy or sell USDT (and USDC) at competitive rates using more than 80 local payment methods across supported countries. Users post or take offers, matching happens inside the platform, and settlement occurs on supported chains such as Arbitrum and TRON.

USD Account: Open a virtual dollar account in the user’s name. Receive international wires or payouts from services like PayPal and Wise directly into the wallet as digital dollars. Intended for salary receipt, client payments, and cross-border inflows without a traditional U.S. bank account.

Stablecoin wallet and exchange: Hold USDT and USDC, swap between local currencies and digital dollars at displayed rates, and send stablecoins or local value to other El Dorado users (free “El Dorado Pay” transfers between app users).

Local spend and transfers: Pay merchants or peers via QR codes in Argentina, Bolivia, Peru, Colombia and via Pix in Brazil. The app bridges the stablecoin side to local rails so the recipient receives what they expect in their preferred method.

Card and future features: An international prepaid Visa card denominated in USD is promoted (issued via U.S. partners, not available to U.S. residents). Full crypto trading and an Earn product are listed as coming soon.

On the infrastructure side, El Dorado has begun offering business accounts and multi-user settlement using Tempo. The funding announcement highlighted real-time settlement for companies handling cross-border flows, including examples like trade in electric vehicles. The consumer app already reaches 12 countries with over one million downloads and tens of thousands of reviews; funding materials cite more than 100,000 active users and over five million transactions processed.

The company was founded in 2022, is based in Bogotá, and is led by CEO Guillermo Goncalvez and CTO Juan Carlos Andreu. It previously raised a $3 million seed in 2024 (Multicoin Capital, Coinbase Ventures, Berkeley SkyDeck) plus an earlier pre-seed.

Analysis: reach, model, and honest caveats

El Dorado’s strength is accessibility. By matching P2P offers against the rails people already use (bank transfers, e-wallets, cash-like methods in some corridors), it lowers the barrier for users who want dollar exposure or cross-border utility without learning DeFi or opening offshore accounts. The named USD Account feature directly targets a common pain: receiving foreign income without the delays and fees of traditional remittance or banking chains.

The recent raise and Tempo integration signal a shift toward serving businesses that want similar rails at scale. On Tempo, companies can open accounts with or without a U.S. entity, which matters for LatAm firms and international counterparties. Early B2B traction is claimed, though independent volume numbers for the new business line are not yet public.

Honest caveats:

This is a platform with custody elements during matching, settlement, and account features. Users transfer stablecoins to specific networks (Arbitrum or TRON per support notes) for deposits; the app then facilitates the local leg. It is not marketed as a pure self-custody wallet where you alone control keys for every balance at all times.

Numbers vary by source: app stores show 1M+ downloads and 4.5 stars from ~50k reviews; funding coverage reports over 100k active users. Liquidity and rate quality in any specific corridor depend on active counterparties on the P2P side.

Card, full crypto trading, and earn features appear limited or forthcoming in current materials. Availability and fees for the Visa product depend on partner banks and local rules.

As with any ramp or matching service, compliance, KYC/AML flows, and limits apply. Support responses in reviews show the company is strict about supported networks to avoid lost deposits.

Competition is active. Other LatAm wallets and fintechs offer overlapping stablecoin and card features. El Dorado’s edge will be P2P rate competitiveness, corridor coverage depth, and execution on the Business product.

Early-stage company risk remains: scaling liquidity, regulatory navigation across jurisdictions, and delivering on the Tempo-powered B2B roadmap are not guaranteed.

The on-chain component still provides transparency advantages over pure correspondent banking. Stablecoin issuers publish attestations, and the public ledger gives users visibility into the long-haul movement that traditional wires never did.

Why Latin America cares

For users in Venezuela, Argentina, and other markets with chronic currency pressure, El Dorado offers a practical way to access and move dollar value using the payment apps and methods they already know. A Venezuelan freelancer can receive payment in digital dollars, hold it without immediate conversion pressure, or cash out locally at market rates via P2P. A Brazilian exporter can pay a supplier in Bolivia or Colombia by converting through stablecoins and delivering via local rails, often with better speed and visibility than bank wires.

The superapp approach also matters for people who want dollars for savings or subscriptions without maintaining a foreign bank account. The USD Account feature and the ability to receive from global services directly address real remittance and payroll use cases. QR and Pix integration means the “last mile” stays in the local payment fabric instead of forcing everyone onto crypto-native UX.

On the self-custody spectrum, El Dorado sits in the middle: users gain more direct control over the stablecoin leg than they have with traditional finance, yet they rely on the platform for matching, fiat conversion, and account services. For many, that trade-off is the point — usable dollar rails without becoming full-time crypto operators.

Takeaway

El Dorado demonstrates how stablecoins are becoming everyday money infrastructure for Latin America rather than a speculative side activity. Its combination of P2P liquidity, local-rail handoff, named dollar accounts, and the new Tempo-backed business push targets the precise friction points that have kept cross-border and dollar access expensive or slow for years.

It is not the only option and it is not risk-free. Users should compare rates and liquidity on the corridors they actually use, understand the custody model and supported networks, and treat volume or savings claims as starting points for their own checks. The Business expansion is early. As with any financial tool, run the numbers on your own flows.

The $9M raise and high-profile backers give it resources to grow, but adoption and retention will depend on consistent execution and corridor depth. For LatAm residents and businesses looking for better ways to hold and move dollars alongside their local systems, El Dorado is worth direct evaluation in the app.

Sources

- El Dorado official site and app listings (eldorado.io, Google Play, App Store)

- Funding coverage: LatamList (June 25, 2026), FinSMEs, Crypto Briefing, LinkedIn announcements from CEO Guillermo Goncalvez

- Tempo project site and partnership references (tempo.xyz)

- Prior coverage: Arbitrum blog on El Dorado stablecoin adoption (2025)

- Company statements on user counts, transaction volume, and product scope