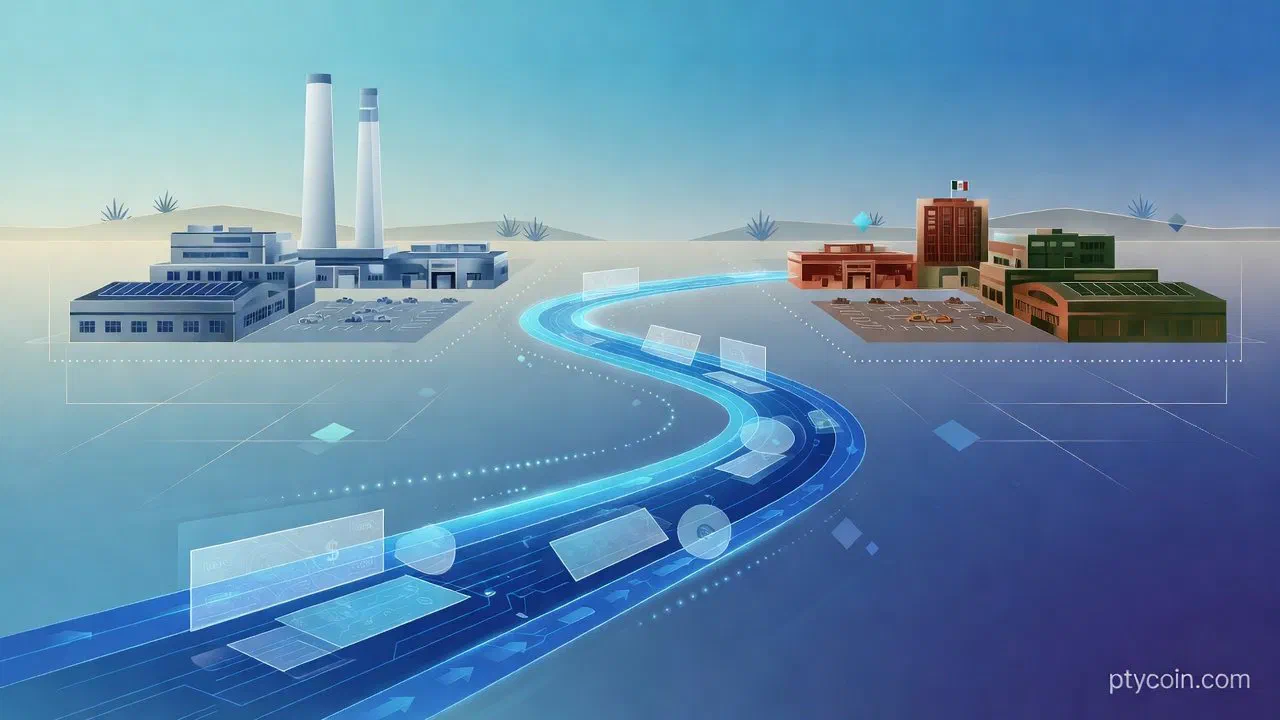

Hyundai Card completed a live stablecoin intercompany transfer on July 9, moving $20,000 from Hyundai Motor America to Hyundai Motor Mexico via Tether’s USDT on Avalanche in about seven minutes. The South Korean card and payments arm of Hyundai Motor Group said the end-to-end cycle, including conversion and verification, beat the three-to-four hours typical of conventional bank wires on the same corridor.

What the pilot actually did

Per Hyundai Card’s announcement and independent coverage from CoinDesk and Crypto Briefing, the first proof of concept ran as a real treasury flow, not a sandbox simulation:

- Hyundai Motor America converted $20,000 into USDT.

- The stablecoin moved on Avalanche to Hyundai Motor Mexico.

- Mexico converted the USDT back into U.S. dollars.

- Transfer plus verification averaged seven minutes.

Partners on the run were Tether (USDT issuer), Avalanche (settlement chain), and Axiym (blockchain payment infrastructure that bridged traditional and on-chain rails). Hyundai Card designed the transfer structure after reviewing accounting, tax, legal, and internal-control requirements at the overseas units, according to the Korea Herald write-up.

The dollar amount is small by automotive treasury standards. The point of the pilot was process, not volume: can a major industrial group settle a real intercompany bill with a dollar stablecoin, keep the books clean, and finish faster than correspondent banking?

Why this is not just another crypto press release

Most stablecoin “pilots” in corporate messaging are still fintech-to-fintech demos or bank sandbox tests. This one is different in three ways that matter for readers watching Latin America.

First, the sender is an industrial conglomerate. Hyundai Motor Group is a car company first. CoinDesk framed the move as the first major South Korean firm to use Avalanche for live cross-border treasury transfers. Permission dynamics matter: when a household brand publicly settles a real intercompany payment on-chain, peer treasurers who have only watched from the sidelines get cover to run their own tests.

Second, the corridor is US→Mexico. Mexico is not a bit player in global auto manufacturing or in regional crypto use. Intercompany flows between U.S. and Mexican subsidiaries (parts, assembly, shared services, shared cash pools) are a daily fact of North American industry. Routing one of those flows through USDT does not remake remittances for families, but it puts stablecoin settlement on a commercial path that already moves large real-economy dollars across the border.

Third, the next step is multi-currency Europe. Hyundai Card said a second PoC among European subsidiaries is scheduled for later this month, with Circle and Visa expected to join. That phase is designed to go beyond dollar-only settlement into local-currency remittances and to measure FX conversion costs, not only speed. If phase one proved the USDT pipe, phase two tests whether the model survives multi-currency accounting and European regulatory reality.

Context: stablecoins as corporate cash, not only retail dollars

Latin America already treats dollar stablecoins as working capital for freelancers, exporters, and households under inflation or capital controls. That retail story is well covered. The industrial version is newer: multi-country manufacturers moving dollars between their own legal entities without waiting on correspondent banks for every small or mid-size transfer.

Traditional intercompany wires are reliable but slow and expensive once you stack FX, nostro/vostro balances, cut-off times, and compliance holds. Seven minutes is a marketing-friendly number; the operational claim underneath is simpler. A treasury team that can settle a verified stablecoin transfer inside a business morning can rebalance cash the same day instead of planning around bank windows.

None of that makes USDT a risk-free bank alternative. Issuer risk, on/off-ramp partners, chain outages, accounting treatment, and multi-jurisdiction money-transmission rules still apply. Hyundai Card’s own framing stresses that the pilot moved past a pure technical check into commercial-deployment readiness, not that group-wide treasury now runs exclusively on-chain.

What to watch next

Three follow-ups will decide whether this stays a one-week headline or becomes a template:

- Europe phase results: local currencies, FX savings claims, and whether Circle/Visa participation is full production tooling or a branded test.

- Scale: $20,000 proves the path; production corridors would need repeated larger tickets, audit trails, and internal policy that survives a bad market day for the stablecoin or the chain.

- Policy perimeter: U.S., Mexican, Korean, and European rules on stablecoin issuance, corporate crypto holdings, and cross-border settlement keep moving. A clean PoC does not freeze any of those rulebooks.

For Mexican and broader LatAm readers, the useful signal is demand from outside crypto-native firms. If auto and other manufacturers keep testing stablecoin treasury on the US–Mexico spine, that is incremental demand for rails, compliance software, and bank partners who can on- and off-ramp without drama. It is not a retail product launch and it is not a price catalyst.

Takeaway

Hyundai Card just showed that a major automaker’s payments arm can settle a real US→Mexico intercompany payment in USDT on Avalanche in minutes, with the books and controls reviewed first. The next European multi-currency test will say more about whether this becomes standard treasury tooling or stays a carefully staged pilot.

Treat it as corporate payments news, not a retail how-to. If you move money for a business across borders, the lesson is to watch settlement time, partner stack, and compliance fit, not to copy a $20,000 PoC into your own books without legal and accounting sign-off. Not financial advice.